Stockholm (9. März 2020, nach Börsenschluß) Stophoist hat in einige „streng vertrauliche“ interne Unterlagen („strictly private and confidential„) von HoistFinance Einblick genommen. Das Datenkonglomerat aus Präsentationen, E-Mail-Kaskaden, handschriftlichen Kommentaren, Memos, Briefen und Vermerken aus dem obersten Management mit Gerichten, externen Steuerberatern und Wirtschaftsprüfern ist auch für Wirtschaftsjournalisten schwer verdauliche Kost.

Es geht hierbei vor allem um die Frage, wie mit der Mehrwertsteuer zwischen den verschiedenen Hoist-Entitäten vor der Integration der deutschen Gesellschaften in den schwedischen Konzern umgegangen werden soll.

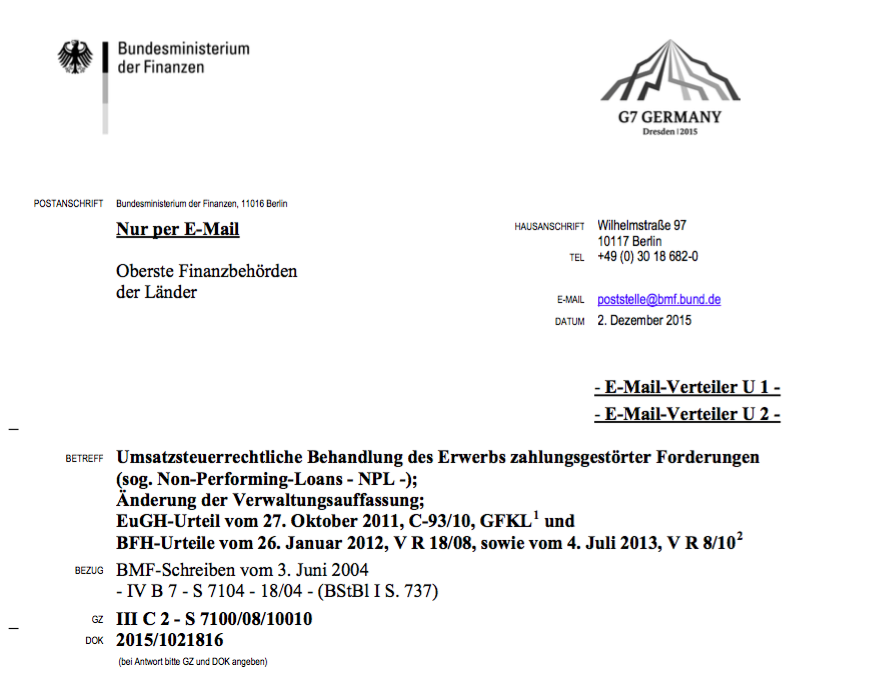

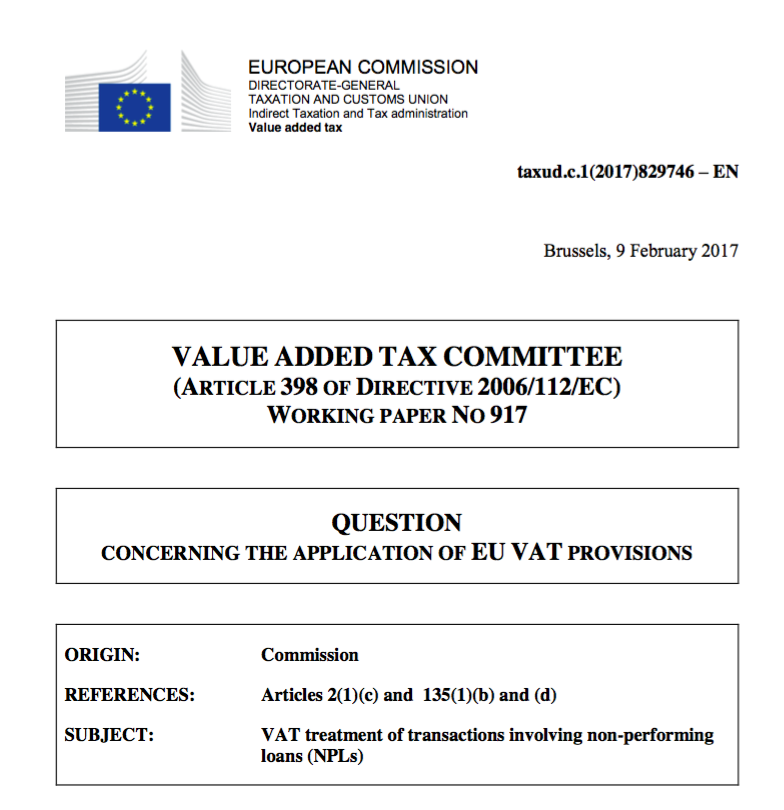

Da es dabei um sehr hohe Summen geht, haben sich auch der Europäische Gerichtshof, das Bundesfinanzministerium und die EU-Kommission damit befaßt:

Was nach dem ersten Eindruck als Bild haften bleibt: Die Hoist-Firmengründer Erik Fällström und Carl Mikael Wirén haben ihr unmoralisches Geschäftsmodell wohl auch auf trickreichen Umgang mit der innereuropäischen Verrechnung der Mehrwertsteuer aufgebaut. Dadurch wurden die Gewinne erhöht, aber auch die Zahlen vor dem Börsengang geschönt. Ob es ein Fall von Prospektbetrug sein könnte, wird noch geprüft.

Über Steuernachzahlungen in Milliardenhöhe als Konsequenz aus dem Umgang der Firmengründer mit der Mehrwertsteuer wurde intern bei Hoist in Duisburg offenbar bereits diskutiert, wie aus dem Entwurf einer Pressemitteilung aus dem Mai 2019 hervorgeht. Eine Pressemitteilung dieser oder ähnlicher Art wurde nie veröffentlicht, aus der Summe der eingesehenen Unterlagen und Kalkulationstabellen sind die darin enthaltenen Zustandsbeschreibungen und Konseqenzen plausibel:

Hoist Finance faces former owners` VAT practice consequences

2019-05-23 23:55

Hoist Finance AB (publ) (“Hoist Finance” or “the Company”) has today announced to the Administrative Court a tax case, in which the Company is involved since German-business model change in 2006. Since than a trust modal was exercised but not followed for Swedish VAT and German tax purposes.

After 2006 Barclays financing related business model changes (assets in shell companies in Jersey, shelter from France and UK corporate taxation, pledged to Barclays), tax opinions had been neglected by former owners and senior management and a VAT scheme between Parent and German was rolled out:

First, do not declare outgoing debt collection services („Profit Share“) to the Swedish parent on German Sub-level. Afterwards, do not declare incoming debt collection services from sub to parent.

Skip reverse charge procedures, save Swedish VAT and rely on false EC-Sales lists and no risk assessment by the financial auditor on VAT riks.

The former Company (HOIST Kredit AB) was obliged to impose Swedish VAT as a service receiver on services rendered by its all its former German entities (Debt Collection Services under the Reverse-Charge-Mechanism, so-called “Profit Share”, as testified by rotating accountants, KPMG and PwC) for the fiscal years 2006-2017 (until HOIST GmbH was merged into HOIST Kredit AB (publ.), leading to non-VATable services between Permanent Establishment and Headquarters.

The matter concerns additional tax and surtax and fines of more than EUR 100 million for the financial years 2006-2017. As non-deductible Swedish VAT was regarded as costs in banking business, EC-Sales list figures have not been filed properly by German service renderers and Swedish service recipients.

The company is willing to take advantage of non-paid Swedish VAT under the statute of limitation as the procedures had been implemented against cross-border tax advice prior business model change by several tax firms. Finally a German Branch was formed to cut VAT recognisable inter-company services.

Several HOIST Management Team members have left the company mostly on short notice after IPO 2015. Hans-Werner Kegel, Sven Krüssel, Uwe-Fritz Albien and Henrik Gustafsson led the German sub HOIST GmbH.

Hoist Finance insists that the company has not followed applicable laws for taxation of its operations in Sweden and Germany by accident, bad management and will appeal any future decision to the Administrative Court of Appeal. The Company believes that it is more likely than not that a financial court will rule in Hoist Finance’s favour. This assessment is also supported by the regular company’s expert adviser who performed pre-IPO tax due diligence. Hoist Finance will be analysing the situation of the pre-IPO shareholders and it will, at a later time, provide information on how the company views laws, rulings and their consequences.

For further information please contact:

Michel Jonson, Group Head of Investor Relations

…

Uwe-Fritz Albien

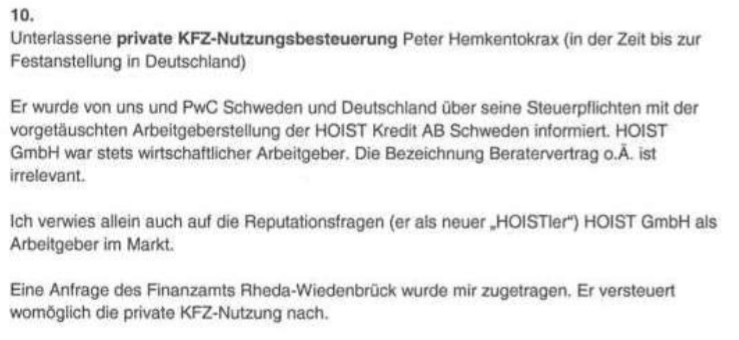

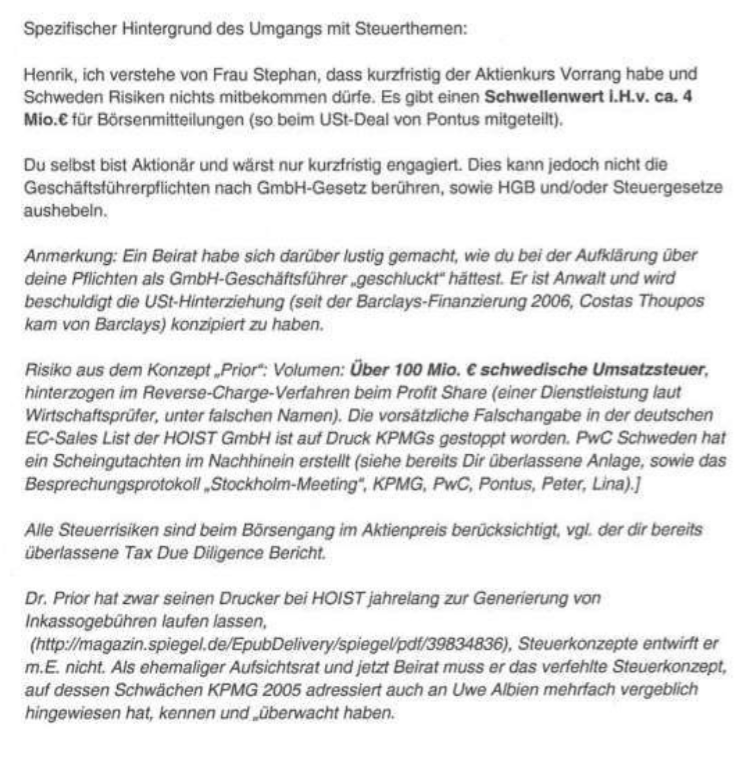

Auch wenn der obige Entwurf einer Pressemitteilung nie veröffentlicht wurde, ist der darin beschriebene Vorgang und Inhalt in Übereinstimmung mit zahlreichen Dokumenten, die aus internen HOIST-Quellen stammen. Ein Beispiel dafür ist ein Memo an Henrik Gustafsson, in dem die Steuerrisikien bei der deutschen HOIST-Tochter aufgeführt werden:

Quelle: HOISTleaksDoc#0812 p 8